Key findings

- Disclosure of carbon credit use is a complicated yet important aspect of corporate reporting as it enables stakeholders to assess a company’s net environmental impact, transition planning and risk exposure.

- Rates of disclosure are already higher than is often assumed, and transparency is set to improve further, driven by new disclosure standards and/or regulations.

- Variations in rules across jurisdictions can add complexity and an extra reporting burden. Dissimilar information may also make it harder for investors to make decisions and report on credit use across their portfolio.

The disclosure of carbon credit use is becoming increasingly important for both companies and investors — but it is also becoming increasingly complicated. The data takes considerable effort to collect and dissect, and there is a lack of standardization in the format and detail of disclosures.

The good news is that, despite these complications, disclosure levels are relatively high. Analysis by MSCI Carbon Markets shows that most companies using carbon credits disclose how many credits they are using — which is not surprising given that one of the aims behind their use is to improve a company’s reputation. Such disclosure allows investors and other stakeholders to assess the credibility of a company’s credit-related claims, as well as their climate targets, transition plans and risk exposures more broadly.

It also helps avoid the same emissions being compensated twice by two companies within the same value chain, or by investors looking to do so for their portfolio — something that might become important if the use of carbon credits towards Scope 3 emissions[1] becomes more widespread. Most notably, the Science Based Targets initiative (SBTi) plans to publish a discussion paper in July exploring such a use case.

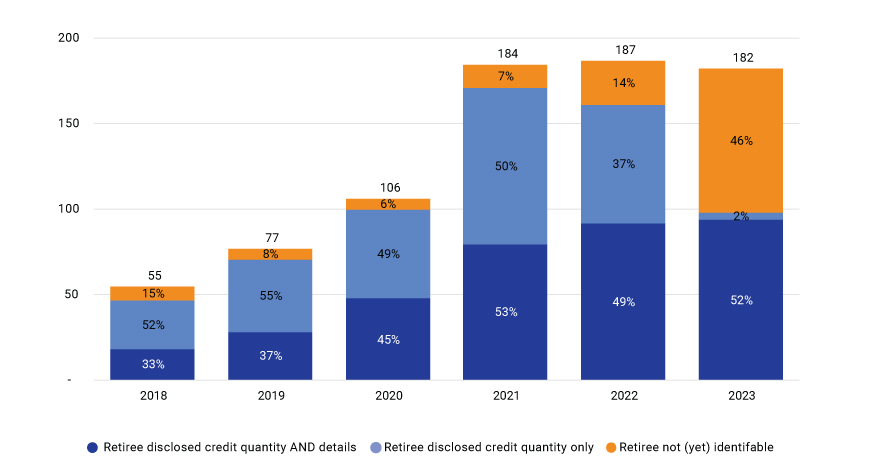

As shown in the exhibit below, some 85% of carbon credits retired since 2018 were attributable to the company using them. Disclosure rates are currently much lower for 2023 due to delays in corporate reporting cycles, but we anticipate this will rise to the 90%-plus levels seen in recent years once such reporting is complete.

When looking at the types of credits used, however, the level of information disclosed falls. Only around half the market reveals the names (and/or unique IDs) of the projects that have generated the carbon credits they are using. In these cases, extensive details on the underlying project can be found on the crediting registry’s website, or via a platform such as MSCI Carbon Markets, including its location, credit methodology and third-party verification checks. Such depth of disclosure is more comprehensive than several other areas of corporate reporting — such as a company’s own emissions or its country-by-country breakdown of employees, taxation or even revenues.

Annual carbon-credit retirements by retiree (MtCO2e)

Data as of March 31, 2024. Source: MSCI Carbon Markets data on corporate credit use, drawn on data published in public company reports, CDP survey responses, press reports and carbon-credit registries (including ACCU, ACR, ART TREES, BioCarbon, CAR, CDM (NDC eligible credits only — excludes other CDM retirements), Climate Forward, EcoRegistry, GCC, Gold Standard, Puro.Earth and Verra).

The push for transparency

Given the above, corporate reporting on carbon credits may not be as lacking in transparency today as commonly assumed — and it stands to get a lot more transparent and consistent.

Registries are an important source of disclosure on the use of carbon credits. To comply with the eligibility criteria of the newly created Integrity Council for the Voluntary Carbon Market’s (ICVCM) Core Carbon Principles (CCPs), registries must require account holders[2] to identify the entity on whose behalf a carbon credit is retired. The ICVCM only requires such information to be disclosed to the registry, not publicly, but this new requirement could lead to higher disclosure rates as this is increasingly seen as good practice.

An equally important source of disclosure is company reporting, which has, to date, largely been made on a voluntary basis. The use of credits was a notable gap in the Taskforce on Climate-related Financial Disclosures (TCFD) disclosure framework when it was finalized in 2017. It has since, however, become common in most new disclosure standards, both regulatory and voluntary.

Regulators in many jurisdictions have begun developing disclosure rules for companies based on recommendations by the International Sustainability Standards Board (ISSB), and many others have signalled that they will do the same. The U.K. plans to integrate the framework developed by the Transition Plan Taskforce (TPT) into its reporting requirements, something that other jurisdictions may follow. Among voluntary standards, almost all now require a company to disclose the carbon credits it is using, or plans to use, if it wishes to make a credit-related claim. As a result, the number of companies disclosing details on their credit use is set to increase.

Unfortunately, knowing what to disclose, in what jurisdiction and to what level of detail, is not a simple matter. The rules are being set in different ways and at different speeds across major markets. These differences may increase reporting burdens for companies, particularly for multinational companies subject to more than one rule, and that dissimilar information may make it harder for investors to take decisions.

Additional challenges for investors

Investors are also being drawn into disclosure requirements. Some regulators may ask investors to disclose information about the use of credits by portfolio companies and ensure that these credits are not counted within an investor’s financed emissions.

Many companies located or operating in the EU will need to comply with the Corporate Sustainability Reporting Directive (CSRD), which asks companies and investors to undertake best efforts to disclose credits used across their supply-chain and portfolios where material. The same may be the case with planned updates to the 2019 EU Sustainable Finance Disclosure Regulation (SFDR). A draft update could introduce provisions for some funds that promote social or environmental characteristics or have sustainable investments as their objective to report the volume and other details of credits retired in relation to a financial product, including those used by investee companies.

Aggregating this information portfolio-wide presents additional challenges, such as data availability and standardization, but also provides greater insight into the investor’s exposure to carbon markets and certain transition risks. In considering such provisions, EU regulators have advised investors to seek support from third-party data providers.[3] To support this need, MSCI has recently launched a CSRD-aligned solution (see here) that can help investors address the complexities of CSRD reporting, including the use of carbon credits.[4]

What exactly needs to be disclosed?

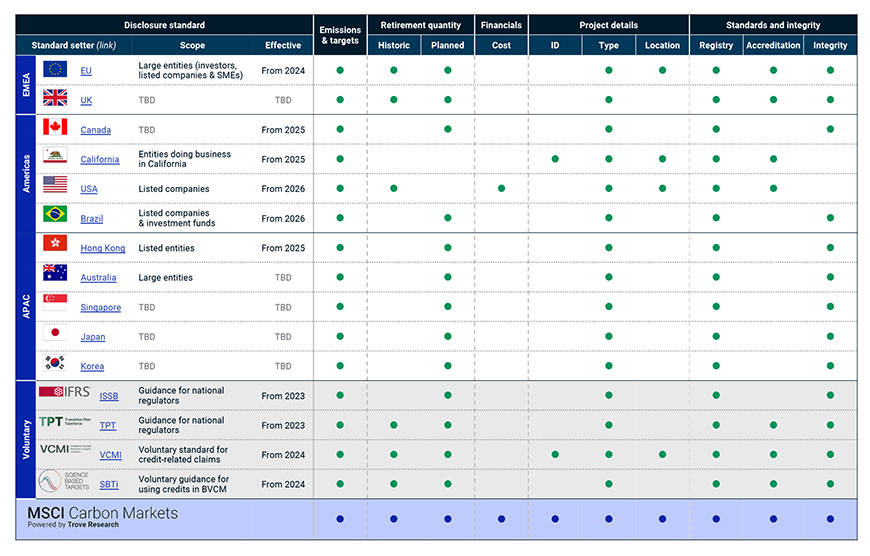

At a high level, the type of information corporates are being asked to disclose is similar across jurisdictions, typically focusing on the quantity of credits used, their type and location, and information about their standards, accreditation and/or integrity. Details, however, differ. Adding to the complexity, many regulations use terminology unfamiliar to carbon-market participants or provide ambiguous requirements, particularly when referring to registries and integrity criteria.

Disclosing the quantity of retired credits allows stakeholders to assess the extent to which credits are used within a company’s climate claim or targets, and form part of its expenditure on climate mitigation. In March, the U.S. Securities and Exchange Commission (SEC) strengthened their climate-disclosure rules, requiring companies to disclose the value of credits expensed and capitalized, where financially material.

However, even on simple-sounding requirements such as the volume of credits retired, different regulations have taken different approaches. Some require companies to disclose current credit use while others ask for planned use of credits. The challenge on the latter is that few companies will be able to say with confidence what credits they plan to retire over long-time horizons — at best they might know a target volume and be able to make a high-level commitment to quality and certain credit types.

Beyond credit quantities, disclosure of the project type is often requested as it can be seen as a good indicator of its expected permanence and co-benefits. Similarly, disclosure of a project’s location is an important factor in considering its contribution to the host country’s national ambition, national accounting and inherent political risk. Disclosures of the certification and integrity of the credits helps in assessing the environmental credibility of the activity and other factors, such as human rights impacts and legal and ethical safeguards.

Summary of required carbon-credit-related disclosures by jurisdiction or voluntary standard

Non-exhaustive and simplified summary of disclosure standards in relation to the use of carbon credits. This information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with legal, regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed. Source: MSCI Carbon Markets

A registry refers to the body which registers projects, issues credits and records transactions. This can help understand whether the credits used are credible, having gone through review. Some standards and jurisdictions reference additional criteria that should factor into assessments of the credit’s integrity, such as the atmospheric permanence of the carbon reduced or removed, the likelihood that the activity would have occurred without revenue from carbon credits and legal and ethical considerations, such as land rights and free, prior and informed consent.

Grasping the keys to the kingdom

Despite this web of requirements, there are some common elements to good disclosure practice:

- Publicly disclose the exact credits being used in the current reporting period along with other necessary details.

- Disclose the quantity and type of credits that may be needed in the future, including offtake agreements, and any third-party quality standards that will be used to ensure credits are of high integrity.

Investors looking to get ahead of the curve in their climate-related disclosures should also start to aggregate, understand and disclose data in relation to carbon-credit use by their portfolio companies.

Footnotes

- Those emissions that occur in a company’s upstream or downstream activities, such as in the use of its products or source materials. ↩

- To retire a carbon credit, most registries require users to register and use a designated account. These “account holders” may be project developers, investors, companies, individuals or consultancies that retire credits on behalf of a client. ↩

- “Final Report on draft Regulatory Technical Standards,” Joint Committee of the European Supervisory Authorities, Dec 4, 2023. ↩

- To learn more about the investment-grade carbon market data and analytics available from MSCI Carbon Markets, please click here. Our product offering includes data feeds covering credit use / expected use for over 10,000 companies, with details provided to support existing and upcoming reporting standards in all major jurisdictions. Additional analysis on a corporate’s credit use includes detailed assessments of the integrity of credits currently being used and estimates of the future volume and cost of credits should it fulfil its current climate commitments. ↩